What Is Chargeback? How To Dispute Chargebacks?

With the advanced technologies, payments have become more convenient; however, payment dispute cases are rising side by side. Chargeback is one of the common disputes that is not just a threat to the customers or cardholders; it is a red flag for the merchants as well.

Having a thorough understanding of chargeback is vital for customers so that they can accurately figure out whether they are eligible to file a chargeback or not. Similarly, a clear concept will help the merchants to understand the tricks to avoid chargebacks. So, let's delve in:

Understanding Chargeback

Chargeback is a money dispute during an online transaction via cards, UPI, etc. It is a reversal claim of a transaction and a customer/cardholder raises it and merchants have to reverse it.

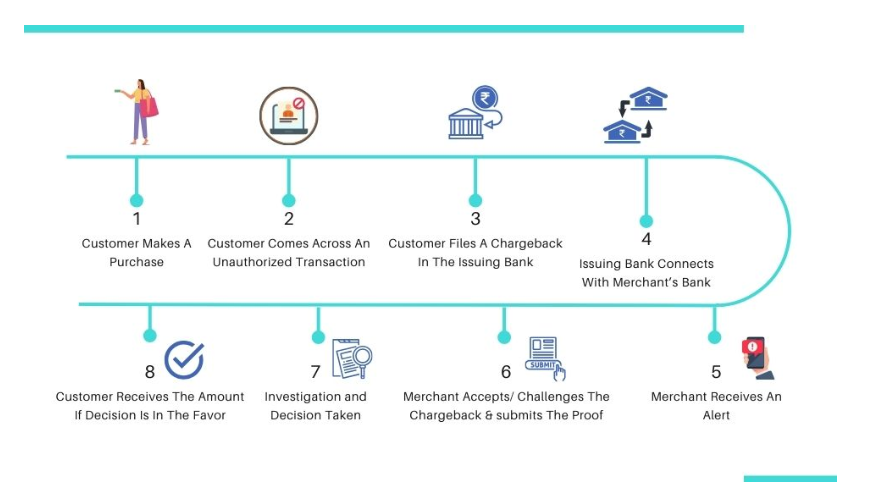

If we break down the problem a bit, a customer reports a payment dispute or files a chargeback complaint on coming across an inaccurate or fraudulent transaction in the issuing bank. On receiving the complaint, the issuing bank first starts to find the genuineness of the complaint. It is called the first level of investigation and on finding the complaint genuine, it registers a chargeback. Then, it goes on forwarding the communication to a merchant's bank and issues a temporary credit in the customer's account (which is debited from the merchant account). If the issuing bank finds that it is truly an unauthorized transaction, that money goes to the customer; else, it comes back to the merchant.

The 3 stages in the process of chargeback are: Chargeback, Pre-arbitration and Arbitration. The final decision is taken and a chargeback is likely to be closed by the Pre-arbitration stage. If it still goes on, the card providers (Visa, MasterCard) come into the matter in the arbitration stage and there will be a processing fee for that - the party losing the chargeback has to pay this amount.

Most Common Chargebacks

Here are the most common types of chargebacks:

1. Fraudulent Chargeback: It occurs when a card is stolen card or the cardholder faced phishing or card fraud.

2. Services/ Merchandize not received: It happens when a merchant fails to deliver the product/service within the promised date or when a customer receives defective product.

3. Credit Not Processed: It occurs when a merchant denies a refund.

4. Duplicate Processing: This is an exceptional case when a customer is charged twice or more for a service. It is possible that customer's attempt is failed; however, the amount got debited every time.

5. Customer does not recognize the transaction: It occurs when a customer finds incorrect billing name in the customer statement from the merchant business name.

Who Is Liable To Pay A Chargeback?

So, the merchant here is liable to pay it back to the cardholders on finding a valid chargeback complaint.

Now, it may sound similar to a refund; however, there are certain differences between these two – have a look into it.

Difference Between Chargeback And Refund

| Chargeback | Refund |

|---|---|

| Initiated by customer through bank | Initiated by customer directly by approaching a merchant - no intervention of bank |

| Customer reports it to issuing bank, and that bank takes this further | On the surface level, it is between customer and merchant |

| The amount collected from merchant and kept on hold until the verdict comes | Initiated amount reaches the customer by the promised date |

| Almost a month-long process | Completed within 7 days |

Why And When Chargeback Requests Are Raised?

The most common causes of chargeback complaints include:

- Any fraudulent transaction

- Unreceived refund for returned item/s

- Shipping and delivery delay

- Payment for a cancelled subscription and many other

A customer may witness an unauthorized transaction (with a known or unknown business), multiple transactions for the same purpose, money deductions for a canceled subscription, etc. Also, a product may not be delivered to the customer, or at the time of paying, the customer may come across a higher payable amount; as a result, they may file a chargeback. In simpler words, customers can raise a chargeback request on finding any money dispute.

How Does Chargeback Work?

How Chargebacks Are Filed?

To file a chargeback, the customer needs to contact the bank directly or call its customer support number and explain the issue. They may ask the customers to fill out a form and submit the documents or transaction ID.

Remember, for different credit cards, there are different time limits to file a chargeback, so check the statements on time and request one as soon as you come across it.

Upon receiving the request, the bank will give a confirmation message. Rarely, a credit card issuer provide a credit amount to the customer on filing a dispute. It mostly happens when the disputed amount is small. In majority of the cases, banks supply the chargeback details to the merchant and give them a time limit to defend it. After getting the response from the merchant, the bank and card provider will make the final decision, which will be sent to both customer and merchant.

While requesting a chargeback, the issuing banks provide the proper reason code based on the guidelines of different card providers.

Click to check the reason codes for:

- MasterCard

- VISA

- American Express

How Long Does It Take To Get The Chargeback Amount Since Filing?

It takes almost a month to get the chargeback – it may take even longer. And only when the merchant agrees with the verdict, the customer will get it.

Chargeback And Merchants

As soon as the customer files the dispute, the merchant will receive a notification and a time limit of 30 days to prove the claim invalid. Also, the merchant gets the transaction ID and the reason customer showed. Merchants can accept or challenge it right there.

On challenging the decision, the merchant needs to

- Submit a rebuttal letter

- Review the charges

- Check for shipment or transportation delay (for which the customer has not received the parcel)

- Check for duplicate payments

If the merchant is clean, he/she can submit screenshots and other supporting documents. On the contrary, the merchants will have to pay a fee along with the requested amount. Even after the final decision, the merchants can appeal through arbitration in case he/she disagrees with the decision.

Fighting Against A Chargeback: Quick Tips To Dispute Chargebacks

No matter what the chargeback amount is, it greatly affects a business's reputation. Sometimes, merchants have to pay the amount back due to the lack of eviden

At the same time, do not compromise with the security during the payment. And, of course, offer multiple payment options (cards, UPI, Net-banking, etc.) to your customers so that not a single customer drops due to the lack of payment options. You can use online payment gateway to receive ultra-secure payments from all your buyers.

Tips To Avoid Chargebacks

1. Use Payment Gateway – One way to fight against it is using a payment gateway. It will minimize chargeback cases, and merchants can maintain their goodwill.

2. Follow the Credit Card Guidelines – A reliable POS can also reduce chargeback cases. Ask the customers to sign the bill for offline card transactions to prevent unrecognized transactions.

3. Make Transparent Business Policies – Ensure order tracking features to get information on any delay in delivery. Mention return and refund policies in clear terms.

Wrapping up…

Though chargebacks were introduced to give more power to the customers, this power is often being misused. Be it a true/legitimate or friendly payment fraud or just some technical/merchant-side issues, chargebacks are frequent. Not all customers are innocent, nor are all of them evil – sometimes, they genuinely fail to recognize a transaction, and some have evil intentions behind it. But all these ultimately affect the merchants because the amount goes from the merchant's pocket. Therefore, securing all credit card purchases is equally essential.